EM Advisory’s Mid-Year Review of the Ghanaian Economy and Projections for the Rest of the Year

Table of Contents

Summary

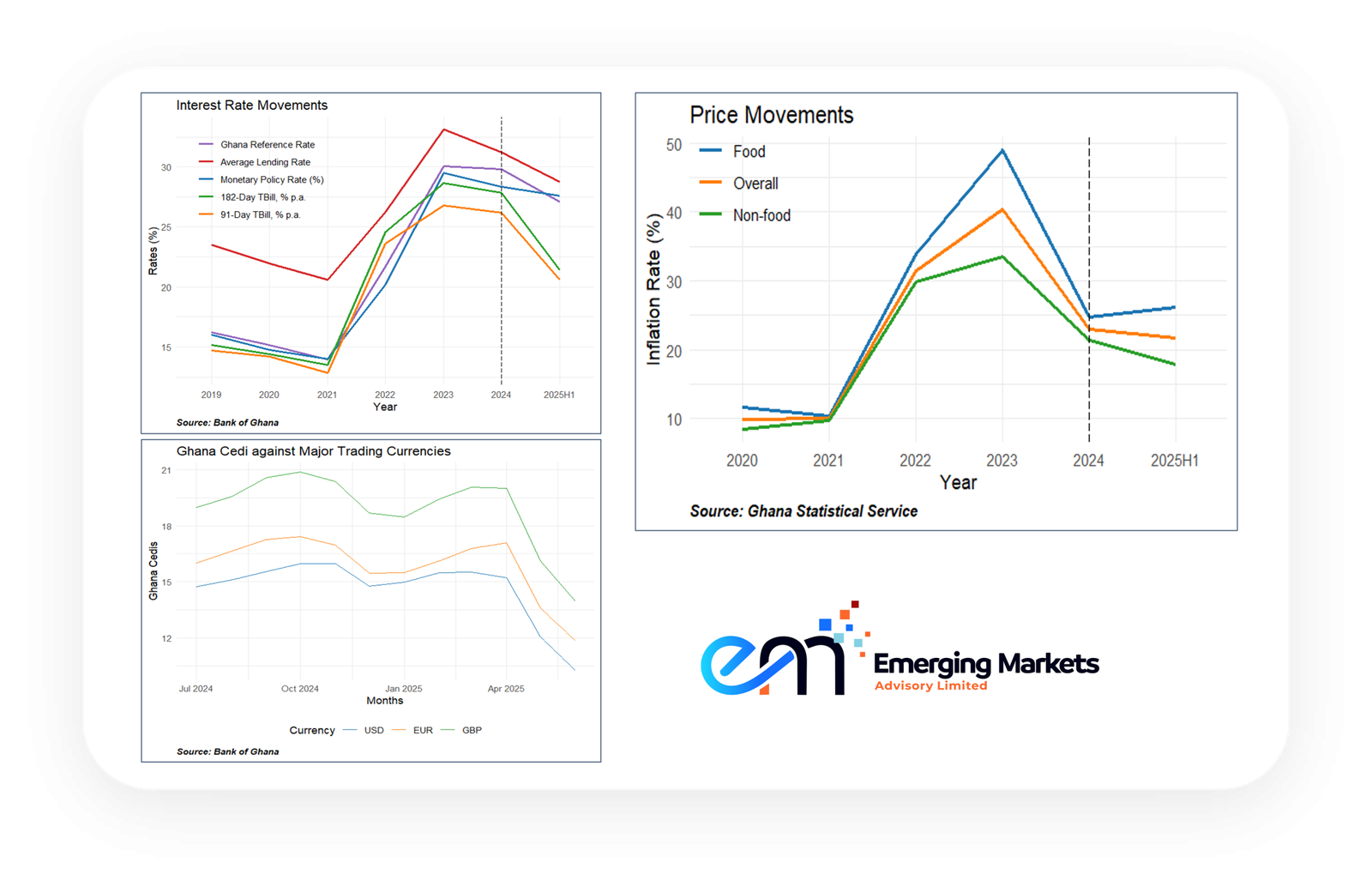

Six months into President Mahama’s second term, Ghana’s economic recovery reads like the story of a near-perfect turnaround. Inflation declined by 10.1 percentage points; the cedi appreciated by 42.6% against the dollar, 30.3% against the British Pound, and 25.6% against the Euro; and most of the fiscal targets for the first half of the year have been met. A 5.3% growth in the first quarter was the fastest Q1 growth since 2020, which represented significant macroeconomic improvement.

However, deeper analysis reveals important nuances. Growth in the agricultural sector has been significant, yet its sustainability is uncertain. Likewise, the dramatic disinflation and currency appreciation appear to be driven by temporary factors. These gains, though impressive, rest on fragile foundations and key growth poles remain exposed to downside risks. The government continues to emphasise fiscal discipline and policy coordination as anchors against mean reversion. Many Ghanaians will welcome this momentum and sincerely hope it endures, but sustaining these gains will require credible reforms, consistent implementation, and a commitment to transparency.

This is not to diminish what has been achieved. But sustainability is the real test. The challenge is to build on these early gains while preparing for the less favourable conditions that inevitably lie ahead.

Following the presentation of the mid-year budget statement, this report examines both the considerable progress made and the risks that remain, offering an independent assessment of where Ghana’s economy truly stands and what needs to happen next.

In a Snapshot …

Between the Lines ...

Some achievements presented by the current administration appear quite outstanding and invite further scrutiny. This is not intended to disparage the administration’s performance, but it appears only logical to assess whether they are only riding on a temporary wave of momentum. Absent the contribution of gold, it is difficult to identify any other plausible source for the robustness of our foreign exchange buffers, which have underpinned this administration’s ability to stabilise the cedi through timely market interventions.

Against this backdrop, it has resulted in a wide divergence in currency value between the Bank of Ghana and off-the-counter values. Additionally, Ghana’s debt restructuring programme over the last two years has contributed largely to lowering the effect of cedi appreciation on the debt stock. A reduction in Ghana’s debt stock has given significant fiscal space to the current Government, enabling it to pursue the fiscal consolidation path it’s been on right from the beginning of the year.

While the measures pursued so far have contributed to stabilising the economy, the question remains of whether Ghanaians are feeling the impact. Electricity prices have increased by 14%, while water prices have risen by 4% since the start of the year. Likewise, a 1-cedi tax on a litre of fuel at the pump has been imposed. There are also signals from the transport sector that transport fares are set to increase by a further 20%. Given the cascading effect of transport prices on all aspects of the economy, the tendency for elevated inflation in the year is high, which may affect the Government’s inability to meet its target for the year.

Moreover, a budget surplus of 1.1% of GDP, while desirable, should be considered in light of certain factors. The government’s posture in the first half of the year has been to spend less, which was easier to accomplish in the first six months because many sympathised with the adjustments of a new administration. But highly characteristic of all new governments, the “grace period” will soon elapse, leading to an infusion of pent-up expectations when people begin to push back and hold the government to its promises, even requiring it to do more. The real questions are whether such impressive figures can be sustained when the cork to fiscal spending is ripped off, whether the new taxes being introduced will adequately address the impending political pressures, and whether expenditure cuts are sufficient to fill the gap left by taxes that have been scrapped.

Lastly, the budget review failed to demonstrate the government’s commitment to funding and completing unfinished projects. In Ghana’s multiparty system, the frequent abandonment of projects when power changes hands has become a troubling norm. Unattended projects should be recognised as a drain on national resources.

The Macroeconomic Scorecard: Real Progress is Evident

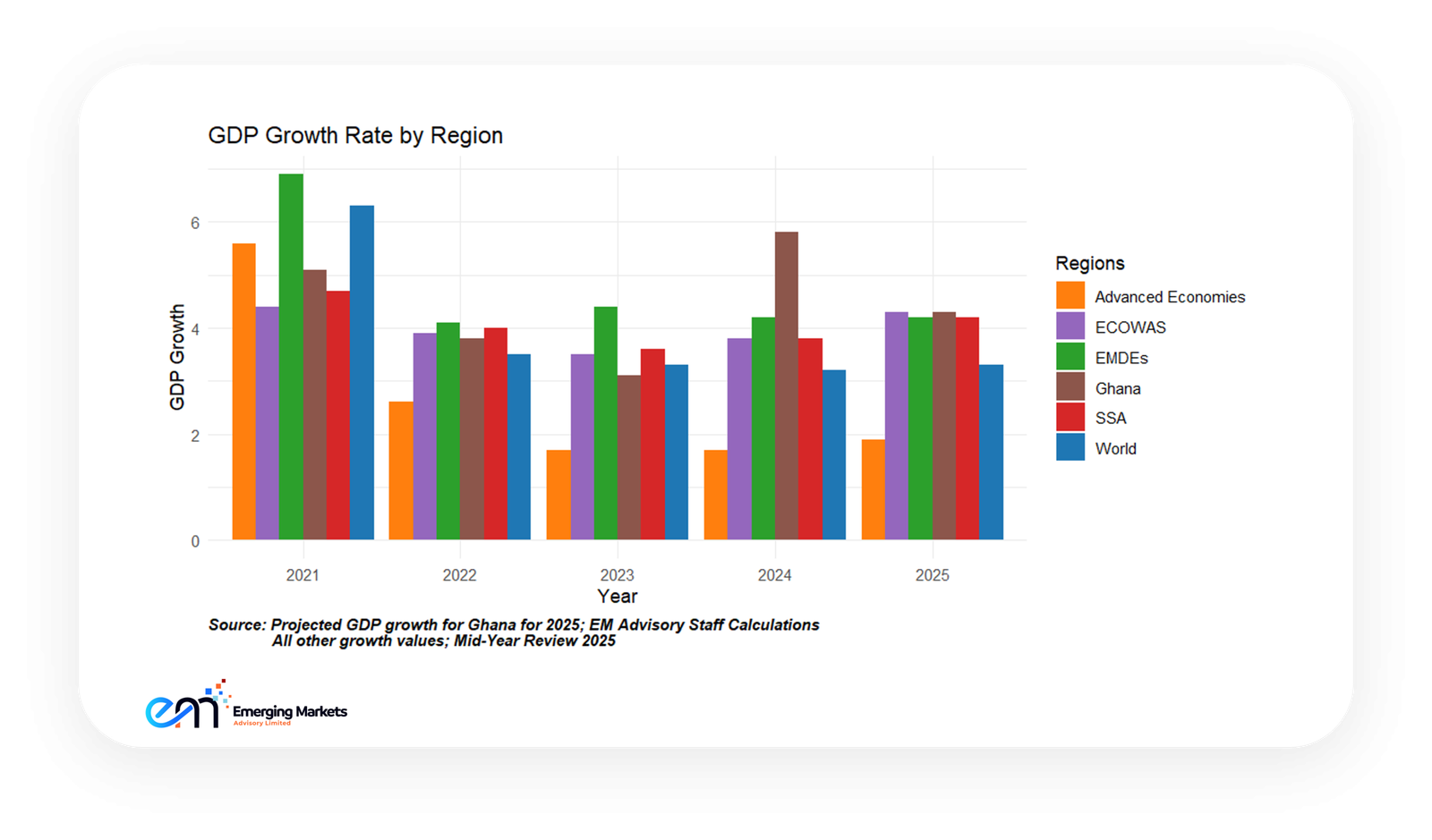

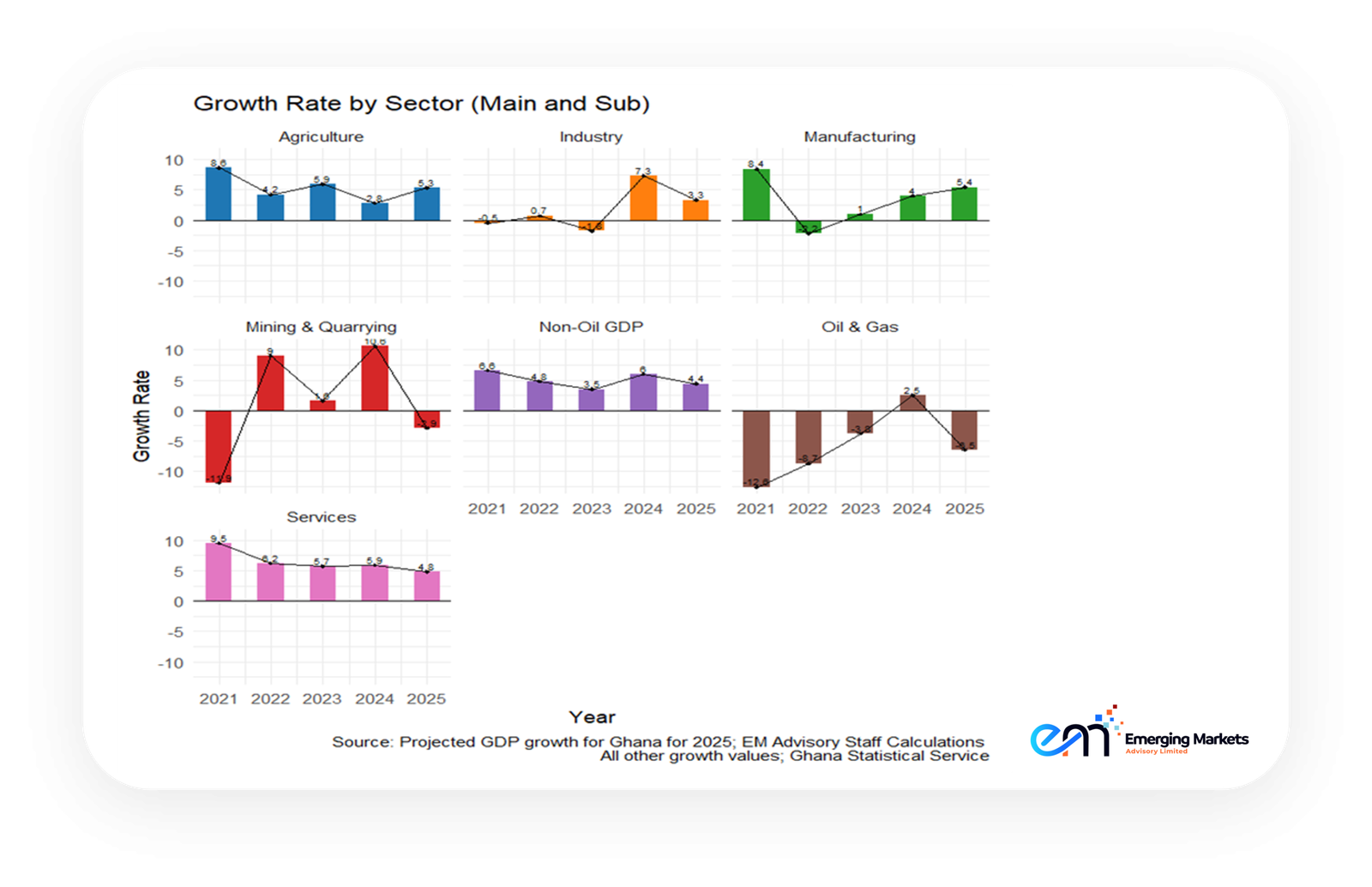

Let us start with what is working. Growth appears robust at 5.3% in the first quarter. The agricultural sector’s 6.6% growth drives much of the GDP improvement, yet there is no discussion of whether this reflects genuine productivity gains or just good fortune. Manufacturing also posted an impressive growth of 6.6%, contributing to a broader recovery in the industry sector after years of successive contractions between 2020 and 2023.

If the government maintains its current trajectory, EM Advisory forecasts that by the end of 2025, the sector will have grown at an average rate of 5.4%, outpacing agriculture and the services sector, which are projected to grow at 5.3% and 4.8% respectively. Despite this strong performance in manufacturing, we anticipate a 3.3% growth rate for the industry sector overall. We believe that the overall sector holds the promise of expanding by 4.3% by the end of 2025 despite contractions in some subsectors, such as mining and quarrying, as well as oil and gas.

However, notwithstanding this sound macroeconomic performance, it is still too early in the new administration’s tenure to suggest that these improvements reflect structural changes, and the real tests will come when favourable conditions reverse. The government’s projections suggest they understand these vulnerabilities, as they are forecasting essentially the same medium-term growth path as their predecessors. That said, the planned rollout of flagship initiatives, such as the 24-Hour Economy Policy, the Big Push Programme, and the Agriculture for Economic Transformation Programme, offers a pathway to more resilient growth, if implementation is disciplined and sustained. That remains the critical challenge.

The Cedi Recovery: Genuinely Unprecedented but Sustainable?

Ask any development economist, and they will confirm that a currency appreciating 42.6% against the US dollar in six months is not something you see every day. The government reports that this unprecedented strengthening has almost reversed all depreciation from 2022 to 2024. If sustained, this could potentially represent one of the most dramatic currency recoveries in the sub-Saharan African region.

What exactly is driving this appreciation? The evidence suggests a confluence of temporary factors: IMF disbursements, which provided confidence; a massive surge in gold exports; rallying gold prices.[1], rising remittances, and significant central bank intervention. The government’s new Gold Board promises to direct more export proceeds through official channels.

However, currency markets are inherently volatile, and sharp appreciations can create their own challenges. The fundamentals that contributed to the 2022-2024 depreciation, i.e., productivity gaps, import dependence, and fiscal pressures, require time to address. The IMF has warned against transitory forex market involvement, instead suggesting a systematic program that will lead to limited footprints in the Forex market, which can anchor expectations and support business in difficult times.

Analysts are also right to ask: What happens when gold prices normalise? Or when the IMF programme concludes? Or when debt service obligations intensify? How does this appreciation impact export competitiveness? This is a space that requires oversight. Currency rallies can be fleeting, but after the battering the cedi has endured in recent years, we genuinely hope this recovery proves durable.

[1] Trading at 3,430.27 USD/t.oz as at July 22, 2025, representing over 42% increase compared to same time last year.

Fiscal Performance: Discipline Today! What about Tomorrow?

The government has delivered impressive fiscal discipline in its first six months. The primary surplus of 1.1% of GDP exceeded the target of 0.4%. Total expenditure came in 14.3% below budget. These numbers represent genuine spending restraint and improved revenue collection that deserve recognition.

However, three significant challenges emerge from the data. First, customs revenue missed targets by GH₵1.6 billion, a shortfall that potentially points to operational challenges at the ports. While the government attributes this to smuggling and corruption, the cedi’s appreciation has also reduced the local currency value of imports, automatically shrinking the customs tax base. This could also be due to lower import volumes resulting from sluggish trade, which is indicative of a general slowdown in economic activities, likely due to the government’s austere policies.

Next is the wage bill, which was overrun by GH₵1.3 billion in just six months. The government attributes this to recruitment decisions made in late 2024, but the overrun also reflects ongoing challenges in payroll management. The discovery of 14,000 unverified workers and 53,311 departed staff still drawing salaries reveals systemic control weaknesses. Payroll audits and clean-up drives have featured in almost every administration’s reform agenda, and yet the problem persists. The recurrence of such issues suggests not just technical lapses, but a more profound institutional reluctance or inability to enforce lasting accountability.

Third, while the government inherited steep debt repayment obligations (GH₵20 billion in 2026, GH₵50.3 billion in 2027, and GH₵45.8 billion in 2028), the recently completed debt restructuring is expected to provide relief. However, post-restructuring debt service could still prove problematic if fiscal discipline is not maintained. History shows that debt restructurings don’t happen only once, and countries that fail to live within their means often find themselves back at the negotiating table. The government’s Sinking Fund would be key to avoiding future crises as it could potentially smooth out future repayment cliffs and avoid renewed fiscal distress.

Revenue Measures to fund the vision

No new revenue measures were announced in the mid-year budget statement, a welcome relief for Ghanaians, particularly following the recent increase in the fuel levy by GH₵1 per litre. In addition, there is now greater clarity on the broad policy direction underpinning the ongoing VAT reforms.

At a minimum, the following key changes were announced by the Finance Minister in the mid-year budget statement:

- The COVID-19 Levy is to be abolished.

- The effective VAT rate is to be reduced.

- The punitive cascading effects of the GETFund and NHIS levies are to be eliminated.

- The VAT Flat Rate Scheme is to be removed, and a unified VAT rate is to be introduced.

- The VAT registration threshold is to be increased to exempt small and micro businesses.

- Compliance to be enhanced through public education, awareness campaigns, and the adoption of fiscal electronic devices (FEDs).

With Ghana’s VAT compliance gap estimated at approximately 80 per cent, these reforms are ambitious and potentially transformative. They aim to reduce tax burdens, simplify compliance processes, enhance equity, and ultimately boost government revenue. However, well-designed tax laws alone will not be sufficient to deliver these outcomes. Their success will hinge on practical implementation and several supporting measures.

First, there must be a full nationwide rollout of the VAT e-invoicing system, alongside the integration of fiscal electronic devices (FEDs) into the Ghana Revenue Authority’s (GRA) core systems. This integration will reduce underreporting, strengthen audit trails, and enhance enforcement. It will also lower compliance costs for both the GRA and taxpayers.

Second, the VAT refund process must be digitised, with clear timelines established to ensure refunds are processed efficiently and cost-effectively. A more predictable and transparent refund system will improve business cash flows and encourage greater compliance.

Third, sector-specific incentives or exemptions should be carefully designed for industries with low profit margins, particularly agriculture, informal retail, and transport, to prevent unintended burdens. These efforts should be paired with continuous monitoring and feedback mechanisms to ensure reforms do not inadvertently trigger price increases or drive economic activity into the informal sector.

Finally, as the VAT Flat Rate Scheme is phased out, it will be essential to introduce a simplified VAT regime that makes formalisation more attractive for small and medium-sized enterprises (SMEs). This step is essential to broaden the VAT base sustainably and inclusively.

The direction of VAT reform is truly encouraging, but its impact will depend on how well these accompanying reforms and safeguards are executed.

The Big Arrears Question

One of the most significant claims in the 2025 budget is that the government inherited GH₵67 billion in arrears from December 2024. It is a substantial figure that helps contextualise the fiscal challenges faced by the new administration. However, this figure requires scrutiny.

The IMF’s March 2025 report offers a different perspective, noting that “a significant share of such payables may not be supported by valid documentation.” The ongoing audit supports this assessment. An amount of GH₵3.6 billion has been rejected outright so far, for errors and non-compliance. Another GH₵562 million lacks proper documentation, and a substantial GH₵27.3 billion remains under validation.

This discrepancy matters for several reasons. First, if the validated arrears figure proves significantly lower than GH₵67 billion, it would indicate a more favourable inherited fiscal position than initially stated. Second, it raises crucial questions about the quality of public financial management systems that allowed such uncertainty about government obligations. The Auditor General’s recent assertion that Ghana’s debt may be overstated by as much as GH₵138 billion further underscores the scale of the problem. Such uncertainty in reported figures undermines fiscal transparency and complicates efforts to rebuild credibility with both domestic and external stakeholders.

The completion of the arrears audit will provide clarity, but the preliminary results suggest caution when using the GH₵67 billion figure as a baseline for assessing fiscal performance. The distinction between claimed and validated arrears has implications for evaluating both the inherited challenges and the current administration’s fiscal achievements. This is a space that warrants close and ongoing scrutiny.

The Implementation Challenge: Capacity Constraints in the Public Sector?

One of the most significant claims in the 2025 budget is that the government inherited GH₵67 billion in arrears from December 2024. It is a substantial figure that helps contextualise the fiscal challenges faced by the new administration. However, this figure requires scrutiny.

The IMF’s March 2025 report offers a different perspective, noting that “a significant share of such payables may not be supported by valid documentation.” The ongoing audit supports this assessment. An amount of GH₵3.6 billion has been rejected outright so far, for errors and non-compliance. Another GH₵562 million lacks proper documentation, and a substantial GH₵27.3 billion remains under validation.

This discrepancy matters for several reasons. First, if the validated arrears figure proves significantly lower than GH₵67 billion, it would indicate a more favourable inherited fiscal position than initially stated. Second, it raises crucial questions about the quality of public financial management systems that allowed such uncertainty about government obligations. The Auditor General’s recent assertion that Ghana’s debt may be overstated by as much as GH₵138 billion further underscores the scale of the problem. Such uncertainty in reported figures undermines fiscal transparency and complicates efforts to rebuild credibility with both domestic and external stakeholders.

The completion of the arrears audit will provide clarity, but the preliminary results suggest caution when using the GH₵67 billion figure as a baseline for assessing fiscal performance. The distinction between claimed and validated arrears has implications for evaluating both the inherited challenges and the current administration’s fiscal achievements. This is a space that warrants close and ongoing scrutiny.

Banking Sector Intervention: The NIB Recapitalisation

The government invested GH₵2.45 billion to recapitalise the National Investment Bank, comprising GH₵450 million in cash, GH₵1.5 billion in bonds, and GH₵500 million of GoG shares in Nestle transferred to the NIB. This intervention successfully raised NIB’s capital adequacy ratio from negative 53.13% to positive 23%, preserving GH₵6.4 billion in deposits and 900 jobs.

This financial intervention is one of many measures to revitalise NIB, such as its recapitalisation under the IMF program in 2024 and an attempt to transfer its oversight to ADB. The recapitalisation demonstrates a commitment to maintaining indigenous banking capacity. However, it also raises questions about broader financial sector stability. The budget acknowledges “significant non-performing loans” persist across the sector despite previous interventions. The focus on a single institution, while necessary, doesn’t address systemic challenges.

The Bank of Ghana will need to assert stronger oversight to prevent a relapse into the pre-financial sector cleanup era, when weak enforcement and regulatory forbearance allowed some institutions to operate well outside prudent norms. Without sustained vigilance, recent gains in sector resilience could quickly erode.

As it stands, the real test will be whether NIB can operate profitably going forward without continued government support, and whether similar interventions will be needed for other financial institutions.

Risk Assessment

The mid-year review’s positive tone should not obscure significant risks to economic stability, including:

Near-term risks (0-12 months):

- Commodity price volatility affecting gold export revenues and fiscal receipts

- Potential reversal of currency appreciation as temporary inflows normalise

- Implementation delays in flagship programmes due to capacity constraints

- Fiscal pressures from political economy factors

Medium-term challenges (1-3 years):

- Debt service obligations rising over the medium term as the government reopens the domestic bond market

- Conclusion of the IMF programme, removing the external policy anchor

- Persistent energy sector deficits requiring sustainable resolution

- Climate-related shocks to agricultural production

Structural vulnerabilities:

- Heavy dependence on gold and cocoa exports for foreign exchange

- Large informal economy limiting revenue mobilisation potential

- Weak project implementation capacity relative to development needs

- Regional security dynamics affecting investment and growth

In truth, sustained economic advancement will require more explicit contingency planning for downside scenarios. As global conditions evolve and domestic vulnerabilities persist, the Mahama administration will need to build credible risk buffers and articulate clear response strategies to reinforce investor confidence and safeguard macroeconomic stability. For now, we can only hope the administration stays the course.

Conclusions: Caught between Stabilisation and Transformation

The Mahama administration deserves credit. Fiscal consolidation is underway, and disinflation has been rapid. Its early achievements show that disciplined, targeted policymaking can yield macroeconomic gains even under challenging conditions.

However, stabilisation is not the same as structural transformation, and the government’s projections make this clear. Despite launching high-profile initiatives, projected medium-term growth remains consistent with that of the previous administration, suggesting limited confidence in these policies to shift the growth trajectory materially. Deep-seated implementation weaknesses and institutional bottlenecks persist in the public sector, regardless of who occupies the political leadership. Concerns about the durability of recent gains persist, but with the right choices, this could still mark the beginning of a more resilient recovery.

We suggest the Government focus on a few critical issues in the next 6 months:

First, bolster the Sinking Fund urgently. Ghana must start pre-emptively saving to cushion future shocks. Crises never announce themselves, and when the next one comes, as it inevitably will, Ghana should be ready to stand on its own. The country’s economic managers must plan for the downside: What happens when gold prices fall? What happens if the cedi weakens? Or if climate shocks affect agriculture? The current budget assumes everything goes right, but experience tells us that will not always be the case.

Second, transformation is necessary, but its success is dependent on addressing fundamental issues. Reforms to the VAT system are welcome, and the message should be simple: live within your means, broaden the tax base, and strengthen enforcement. There is no shame in economic simplicity; it is often the best path to stability.

To ensure macroeconomic gains translate into tangible microeconomic benefits for the average Ghanaian, the government must address the gap between high-level stability and on-the-ground realities. While disinflationary momentum is a significant achievement, prices are often sticky downwards, meaning reductions in inflation do not always lead to lower costs for consumers. To mitigate this, the government should explore targeted price regulation mechanisms, particularly for essential goods and services, to ease the cost-of-living burden. Measures such as strengthening consumer protection agencies, promoting competition in key markets, and incentivising price adjustments in response to macroeconomic improvements can help ensure that gains are not only reflected in paper gains.

Additionally, capital expenditure must be rigorously reviewed to prioritise projects with clear, measurable returns that can support debt repayment. With Ghana’s debt obligations looming, investments should focus on high-impact, revenue-generating initiatives, including infrastructure that boosts agricultural productivity or export capacity, ensuring that borrowed funds contribute to sustainable growth rather than future fiscal strain.

Stabilisation has bought time, but time alone will not solve Ghana’s problems. Without tackling deep structural issues such as export concentration, implementation shortfalls, energy sector inefficiencies, and persistent debt risks, the country risks falling back into its familiar boom-bust cycle. The next six months will be decisive. They will show whether this administration dares to move beyond short-term fixes toward real reform, or whether it will merely manage decline more competently than its predecessors.

A more substantial commitment to evidence-based policymaking will be essential. Identify what works, scale it up, and phase out flashy but ineffective programmes that drain resources without delivering impact. Just as importantly, push for a culture of delivery across the public sector; policies are only as good as their execution. Ministries, departments, and agencies must be held to higher standards of performance, reporting, and accountability. Transformation will not happen unless the engine of the state is made to deliver.

The stakes are high. The IMF programme has a shelf life, and the political calendar is steadily ticking toward the 2028 elections. But after years of economic hardship, Ghanaians deserve more than better-managed crises. They deserve a credible, sustainable path to prosperity. Whether this government can deliver remains to be seen, but the signs are there that they are certainly on the right track.