Ghana’s export sector remains a very significant contributor to economic growth. In 2024, exports made up approximately one-third of Ghana’s GDP. This underscores the need for serious attention to export-related issues.

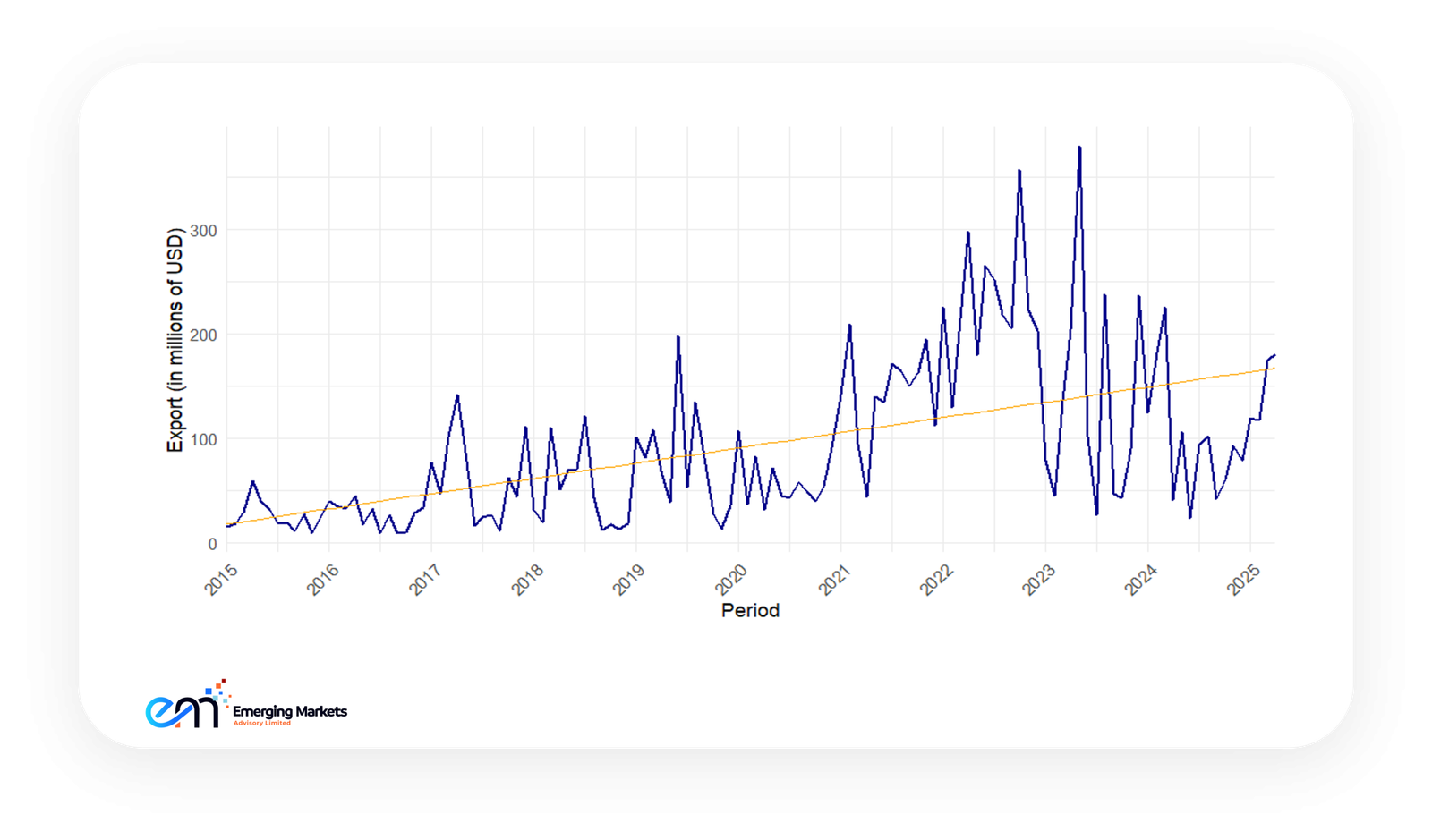

Figure 1: Ghana’s Exports to the US between 2015 and 2025

As Figure 1 shows, over the past decade, exports to the United States have generally trended upwards, despite occasional dips reflecting adverse global events. In March 2025, a month before the imposition of the 10% tariff, Ghana’s export to the United States was $174.77m (inclusive of insurance, freight and other related transportation cost). Barring trade disruptions caused by the 10% baseline tariff, our projections indicate that Ghana’s exports to the United States from May 2025 to April 2026 are estimated at $1.103 billion. This corresponds to an annual growth of 2.81% in exports from May 2024 to April 2025.

As Figure 1 shows, over the past decade, exports to the United States have generally trended upwards, despite occasional dips reflecting adverse global events. In March 2025, a month before the imposition of the 10% tariff, Ghana’s export to the United States was $174.77m (inclusive of insurance, freight and other related transportation cost). Barring trade disruptions caused by the 10% baseline tariff, our projections indicate that Ghana’s exports to the United States from May 2025 to April 2026 are estimated at $1.103 billion. This corresponds to an annual growth of 2.81% in exports from May 2024 to April 2025.

With the 10% tariff increase and based on the United States. trade elasticity of 2.1, we estimate that Ghana’s export demand to the United States is likely to fall by a total of $231.74m by April 2026 (i.e., a year after the 10% tariff imposition). While this figure may appear insignificant (i.e., less than 1% of Ghana’s total exports in 2024), it is not to be taken lightly. Holding all else fixed, EM Advisory further projects that export demand from the United States market will fall by $237.06m, $237.68m, $238.87m, and $240.1m, on average, in the subsequent second to fifth years after the tariff imposition.

This should gravely concern Ghanaian exporters who have not been able to geographically diversify their international trading markets and only target the United States market. Also, exporters who do not export to the United States can still be affected by some redistribution effects. For instance, the fall in United States demand for Ghanaian exports can induce some factor movement into unaffected sectors, thereby bringing down factor payments such as wages and rental costs in those sectors. Ghana should be concerned about the indirect effects of the United States inward-looking trade policies.

As a large country, the trade diversion that would occur can trigger global inflationary pressures, at least in the short run, and slow down real global economic growth. This situation undoubtedly worsens when other large economies decide to retaliate.

On a disaggregated level, the cocoa export subsector is projected to bear the brunt of the tariffs. This is because ‘cocoa and cocoa preparations’ exports have accounted for approximately 51% of overall shipments to the United States in the last decade, on average. This is followed by the ‘mineral fuels, oils, and distillation’ exports, which accounted for 35% of exports to the United States. Exports for all other subsectors put together only make up an average share of 5% of exports to the United States.

Even though these export cutbacks are minor in the grand scheme of things, they have the potential to exacerbate national inequality.

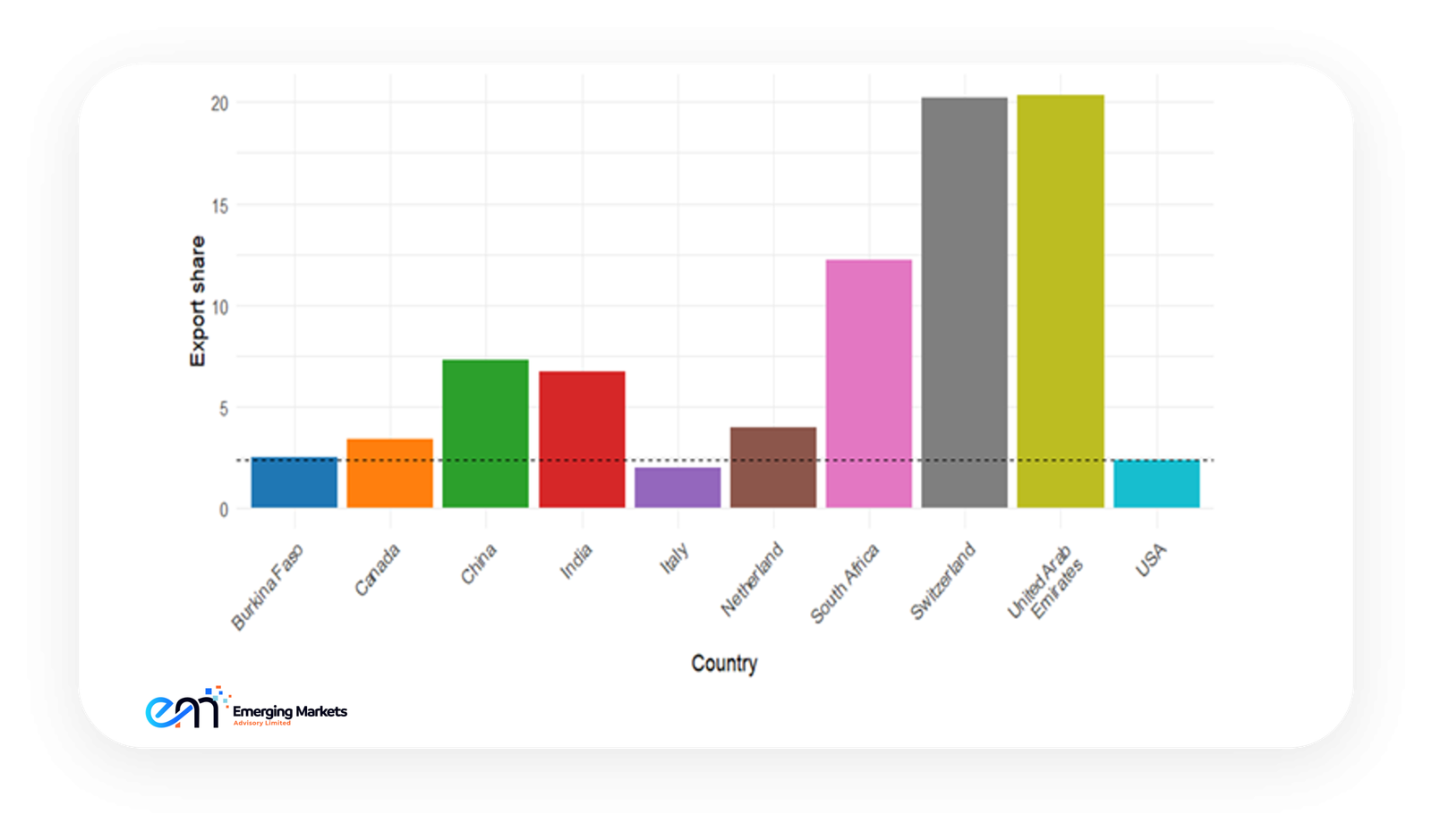

Despite the 10% uniform tax that applies to all Ghanaian products, AGOA allows for a few exemptions. Natural rubber, wood, and oil exports that satisfy the stipulated standards by the United States. are exempted from the tariff under the agreement. While these exempted products account for a small fraction of Ghana’s exports to the United States, they serve to mitigate the total impact of the tariff on the Ghanaian economy. In 2024, only around 2.4% of Ghana’s total exports went to the United States. United States and Canada combined accounted for only 6% of Ghana’s exports, making North America the fourth-largest regional destination for Ghana’s exports, after Asia, Europe, and Africa.

Figure 2: Shares of Ghana’s Exports to the Top ten Significant Destinations in 2024

We believe that it would be unnecessary for Ghana to consider retaliatory actions, as doing so would result in more losses than gains. Ghana’s economy is small and open, and it cannot influence global prices significantly. Imposing greater tariffs on the United States would lead to domestic inflation. As a short-term remedy, Ghana should scale down its exports to the United States and instead focus on its key trade partners, that is, the United Arab Emirates, Switzerland, South Africa, China, and the Netherlands, where the tariffs on Ghana’s exports will be more favorable.